Major factors contributing to the consolidated financial result

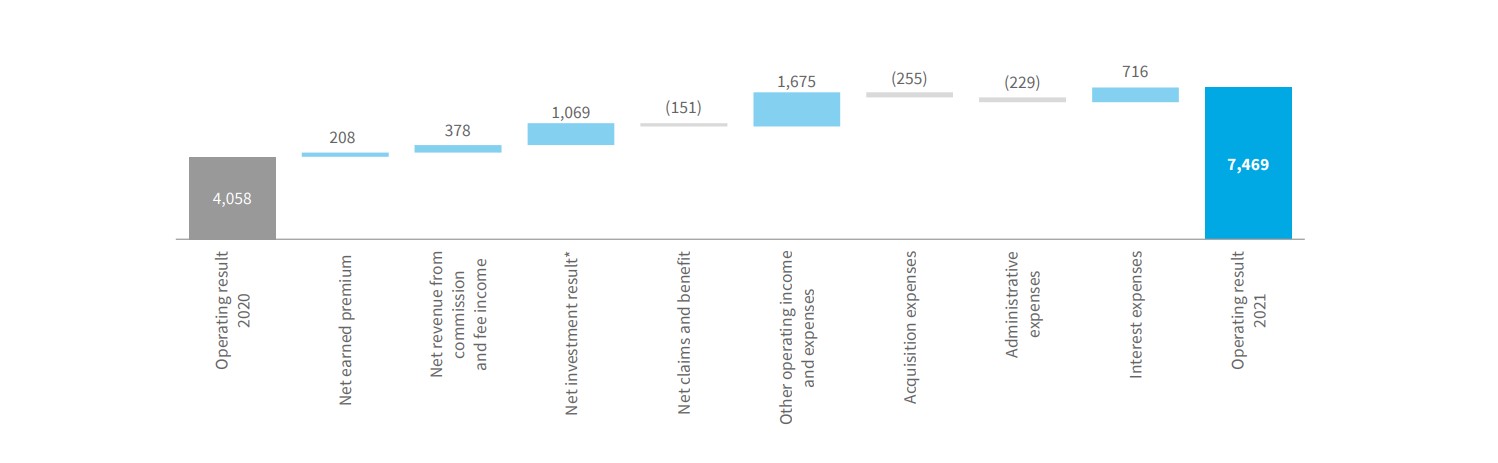

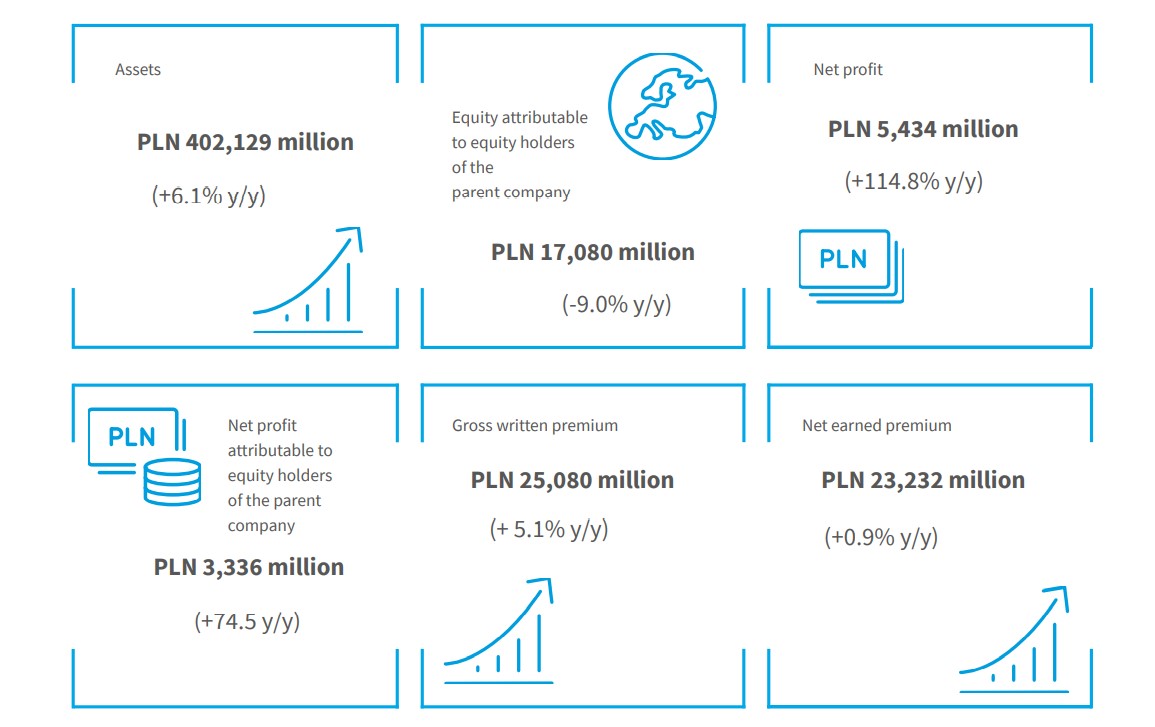

In 2021, net profit attributable to the shareholders of the PZU Group’s parent company was PLN 3,336 million, compared to PLN 1,912 million in 2020 (up 74.5%). Net profit reached PLN 5,434 million, i.e. PLN 2,904 million more than in 2020, and profit before tax stood at PLN 7,454 million, compared to PLN 4,058 million the year before.

Net result rose by 27.3% compared to last year, net of non-recurring events1.

Operating profit in 2021 was PLN 7,469 million, up PLN 84.1 % compared to the result in 2020.

Operating profit was driven in particular by the following:

- higher gross written premium, especially in non-motor insurance and MOD insurance in the mass client segment and corporate client segment, individual protection products in the bancassurance channel, and growth of sales in the Baltic companies, including property, MOD and health insurance products;

- increased valuation of shares in a logistics company following its IPO;

- better performance of the banking business: last year, there was a one-off effect of the impairment losses on goodwill arising from the acquisition of Alior Bank (PLN 746 million) and Bank Pekao (PLN 555 million) coupled with a lower than last year costs of risk stemming from the recognition of additional provisions for expected credit losses;

- lower profitability in group and individually continued insurance, on account of the increased loss ratio due to deaths of the insured and co-insured in the group protection portfolio and in continued insurance;

- higher result in individual insurance achieved on a growing protection products portfolio in the bancassurance channel and term products sold in the own network, as well as higher insurance activity expenses;

- lower profitability in the mass insurance segment, which was an effect of a lower net earned premium, combined with higher loss ratio in motor insurance and higher acquisition expense ratio;

- lower operating result in the corporate client segment, which is an outcome of a decrease in motor insurance profitability, coupled with a lower loss ratio in the non-motor insurance portfolio, including natural catastrophe insurance, third party liability insurance, and insurance against various financial risks.

In the individual operating result items, the PZU Group posted:

- increase in gross written premium by 5.1% to PLN 25,080 million. It concerned mainly non-motor insurance, including insurance against fire and other damage to property in the corporate client segment, as a consequence of renewal of a long-term high-ticket contract and a higher premium written under a contract with a client from the fuel and energy sector, as well as other TPL and ADD insurance and other insurance in the mass client segment, including mainly accident insurance added to mortgage and cash loans thanks to the development of sales in cooperation with the Group's banks. At the same time, a higher premium was posted in MOD insurance in both segments, which is an effect of the gradual revival of new automobile sales after the slowdown caused by the COVID-19 pandemic. In life insurance, the higher sales are attributable to individual protection products in the bancassurance channel; the growth of sales in the Baltic companies was generated by property, MOD and health insurance products. Allowing for the reinsurers’ share and movement in the provision for unearned premiums, the net earned premium was PLN 23,232 million, and was 0.9% higher than in 2020;

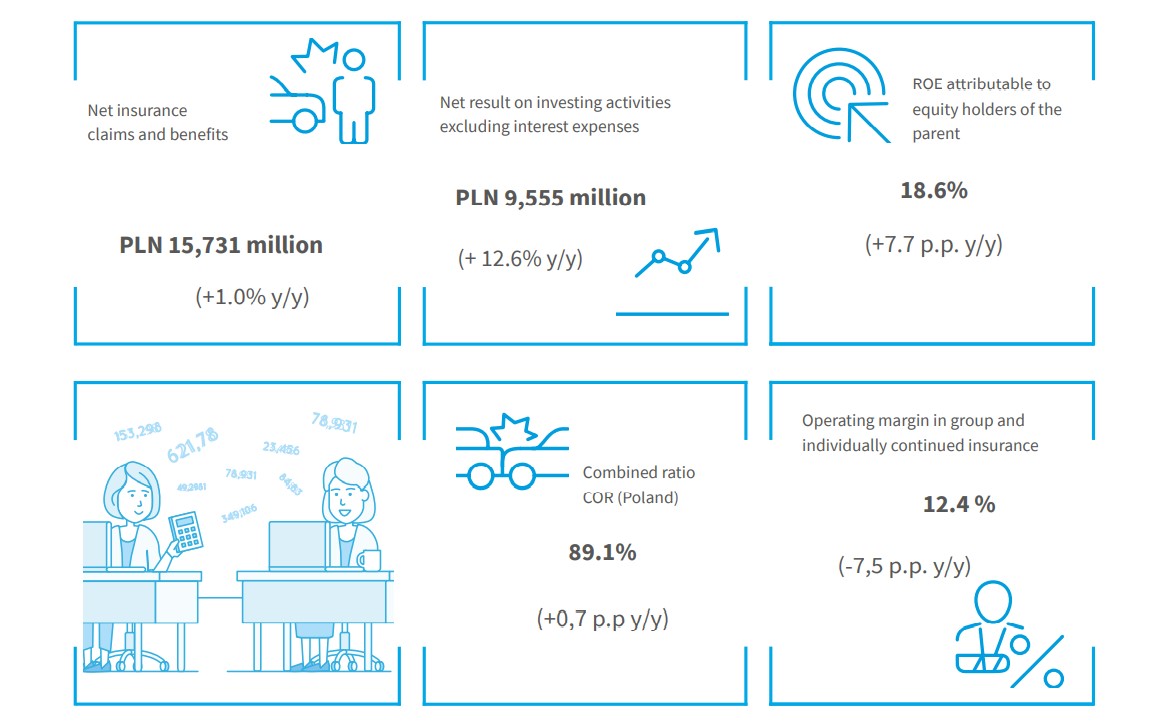

- increase by 24.3% in investment income which, after factoring in the interest expenses2 amounted to PLN 9,137 million, as compared to PLN 7,352 million in 2020. Growth was posted in investment income from banking activity. In banking activity, the increase in profit was triggered by the lower costs of risk due to last year’s establishment of additional loan provisions for the anticipated deterioration in the quality of the loan portfolio in Bank Pekao and Alior Bank. Concurrently, interest income of both banks fell y/y as a result of the low level of interest rates persisting in the first three quarters. Income on investing activity, excluding banking business, fell by 1.6% as compared to the previous year, as an outcome of a lower investment activity result earned on the portfolio of assets held to cover investment products, offset by a better result on listed equities, in particular the higher valuation of the logistics company as a result of its listing on the stock exchange. The positive effect was also enhanced by the high result on the real property portfolio. Lower investment results of the portfolio of assets held to cover the investment products alone do not affect the PZU Group’s overall net result, because they are offset by the movement in net insurance claims and benefits;

- the higher level of claims and benefits paid, which amounted to PLN 15,731 million, i.e. 1.0% more than in 2020. This growth was attributable primarily to life insurance, as a result of the increase in benefits for the insureds’ and co-insureds’ death in 2021, which is correlated with the frequency of these events in the overall population according to the data published by Statistics Poland (GUS);

- acquisition expenses higher by 7.7%, having increased to PLN 3,572 million, from PLN 3,317 million in 2020. This increase is mainly attributable to the modification in the product and sales channel mix, including a higher share of the multiagency and bancassurance channels in the mass client segment;

- increase of administrative expenses by 3.5% to PLN 6,826 million, from PLN 6,597 million in 2020. In the banking activity segment (net of adjustments on account of valuation of assets and liabilities to fair value), administrative expenses increased by PLN 295 million; in the insurance activity segments in Poland, administrative expenses increased by PLN 45 million, which resulted from, among others, increased personnel costs associated with the payroll pressure, intensification of marketing activities, and higher real property maintenance expenses resulting from the indexation of lease hire rents and costs of utilities;

- movement in the negative balance of other operating income and expenses – to PLN 2,315 million, compared with PLN 3,990 million in 2020. This resulted mainly from the non-recurring effects from last year – i.e. the impairment loss on goodwill arising from the acquisition of Alior Bank (PLN 746 million) and Bank Pekao (PLN 555 million), the impairment loss on assets arising from the acquisition of Alior Bank (i.e. trademark and relations with clients) in the amount of PLN 161 million, and the decrease of the BFG contribution from PLN 541 million in 2020 to PLN 396 million in 2021, respectively. At the same time, the burden related to the levy on financial institutions increased (the outcome of growth of the value of assets subject to the levy, and not the rate of the levy).

| Key data from the consolidated profit and loss account | 2017 | 2018 | 2019 | 2020 | 2021 |

| in PLN m | in PLN m | in PLN m | in PLN m | in PLN m | |

| Gross written premiums | 22 847 | 23 470 | 24 191 | 23 866 | 25 080 |

| Net earned premium | 21 354 | 22 350 | 23 090 | 23 040 | 23 232 |

| Net revenues from commissions and fees | 2 312 | 3 355 | 3 279 | 3 166 | 3 544 |

| Net investment result* | 7 893 | 9 931 | 11 298 | 8 486 | 9 555 |

| Net insurance claims and benefits | -14 941 | -14 563 | -15 695 | -15 580 | -15 731 |

| Acquisition expenses | -2 901 | -3 130 | -3 363 | -3 317 | -3 572 |

| Administrative expenses | -5 357 | -6 609 | -6 606 | -6 597 | -6 826 |

| Interest expenses | -1 350 | -2 046 | -2 129 | -1 134 | -418 |

| Other operating income and expenses | -1 552 | -2 201 | -2 790 | -3 990 | -2 315 |

| Operating profit (loss) | 5 458 | 7 087 | 7 084 | 4 058 | 7 469 |

| Share in net profit (loss) of entities measured by the equity method | 16 | -1 | -4 | - | -15 |

| Profit (loss) before tax | 5 474 | 7 086 | 7 080 | 4 058 | 7 454 |

| Income tax | -1 289 | -1 718 | -1 895 | -1 528 | -2 020 |

| Net profit (loss) | 4 185 | 5 368 | 5 185 | 2 530 | 5 434 |

| Net profit (loss) attributable to equity holders of the parent company | 2 895 | 3 213 | 3 295 | 1 912 | 3 336 |

restated data for 2017-2019

* including: interest income calculated using the effective interest rate, other net investment income, result on derecognition of financial instruments and investments, movement in allowances for expected credit losses and impairment losses on financial instruments, net movement in fair value of assets and liabilities measured at fair value

Operating result of the PZU Group in 2021 (PLN million)

* net of interest expenses

1 Non-recurring events include: higher result on investment activity as a result of listing of a company from the logistics industry from a mutual fund portfolio managed by TFI PZU, and last year – the impairment loss on goodwill arising from the acquisition of Alior Bank (PLN 746 million) and Bank Pekao (PLN 555 million), the impairment loss on assets arising from the acquisition of Alior Bank (i.e. trademark and relations with clients) in the amount of PLN 161 million (after adjustment for the impact of deferred income tax and minority shareholdings, the impact on the net result attributable to the parent company’s shareholders was PLN 42 million).

2 Including: interest income calculated using the effective interest rate, other net investment income, result on derecognition of financial instruments and investments, movement in allowances for expected credit losses and impairment losses on financial instruments, net movement in fair value of assets and liabilities measured at fair value, and interest expenses.