Situation on the financial markets

The course of the COVID-19 pandemic, the rising inflationary expectations and GDP growth prospects in Poland and globally were the main factors affecting the financial markets in 2021. The improvement in market sentiments was supported by the unprecedented scale of fiscal and monetary stimuli to combat adverse economic effects of the pandemic. The progress of vaccination against SARS-CoV-2, and the increased resilience of economies to successive waves of the pandemic and the impact of the resulting sanitary restrictions, have also helped to significantly reduce the scale of uncertainty in financial markets. However, the main risk factor remains the further evolution of inflation in the context of possible continuation of disruptions in global supply chains or the evolution of energy commodity prices (also under the influence of the recent escalation of geopolitical tensions).

Bond market

In 2021, the yields on Polish 1-year, 2-year, 5-year and 10-year treasury bonds increased. 1-year yields increased from 0.051% to 3.466%, 2-year yields from 0.102% to 3.346%, 5-year yields from 0.471% to 3.988% and 10-year yields rose from 1.252% to 3.705% (Refinitiv data). The spread versus 10-year German bonds that at the end of 2020 was 183 basis points, increased to 388.9 basis points at the end of 2021 (Refinitiv data). The entire Polish curve moved sharply upwards due to economic recovery, a strong increase in inflation and inflation expectations, as well as rapid and significant NBP interest rates hikes in Q4.

Treasury bonds yields in 2021 (Refinitiv Datastream data)

The NBP reference rate, which was only 0.1% for the first three quarters of 2021, rose to 1.75% between October and the end of December. The situation on the core markets in 2021 also contributed to the increased yields on Polish bonds. Yields on 10-year US Treasury bonds, influenced by rising inflation expectations, increased from 0.9165% to 1.498%, and on German bonds from -0.575% to -0.179% (Refinitiv data).

Equity market

In 2021, the WIG20 index increased by 14.3%, the WIG index by 21.5%, the mWIG40 by approx. 33.1%, and the sWIG80 by 24.6% (Warsaw Stock Exchange data). In addition to the dynamic economic growth and the higher resilience of the national economy to the impact of sanitary restrictions, compared to that observed in 2020, the rises in domestic stock market indices were also fostered by the loose fiscal policy (and a large scale of government aid to businesses in connection with the COVID-19 pandemic) and monetary policy. The low interest rates in an inflationary environment provided an additional incentive for investors in the domestic stock markets. They were also supported by rising risk appetites across the world, usually favoring emerging stock markets, including the Polish market.

WIG and WIG20 indices (Warsaw Stock Exchange data)

In 2021, global equity markets recorded significant gains, caused by growing expectations for economic recovery (prospects of the end of the pandemic and the progress in COVID-19 vaccinations) and increase in inflation (loose monetary and fiscal policy globally). In 2021, the American S&P500 stock index shot up 26.9% (S&P) while the German DAX index climbed 14.0% (Deutsche Boerse). The rising yields did not hinder the growth of stock market indices. Some signs of a slowdown in the growth of stock indices were visible only in China, which was linked to growing market concerns regarding the effect of the gradual phasing out of the intensive economic stimulus programs, previously implemented in China in connection with the COVID-19 pandemic, problems of Chinese real estate developers and the threat of withdrawal of Chinese suppliers from global supply chains. As a result, in 2021 the aforementioned index increased by a mere 4.8%.

Currency market

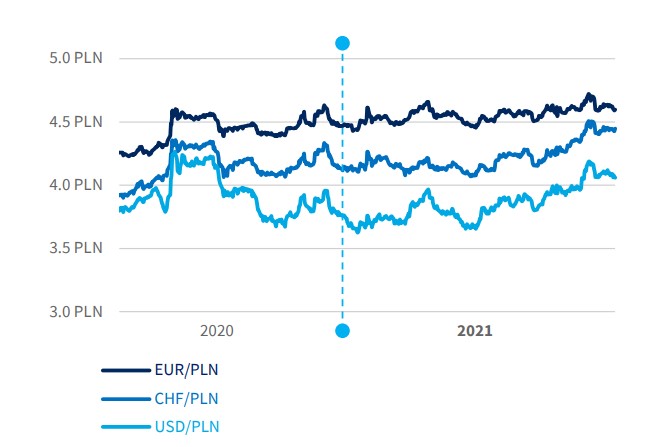

The EUR to PLN exchange rate decreased slightly from 4.61 at the end of 2020 to 4.60 at the end of 2021 (NBP). The key factor, which kept the Zloty at relative weak levels in 2021, was the loose monetary policy adopted by the NBP, which, combined with the steadily growing inflation, led to interest rates in Poland that were negative in real terms. The NBP rate hikes that took place in Q4 did not lead to a significant appreciation of the zloty against the euro. The euro to USD exchange rate fell from 1.23 at the end of 2020 to 1.13 at the end of 2021 (the EUR to USD exchange rate calculated on the basis of NBP EUR/PLN and USD/PLN exchange rates). The strengthening of the dollar resulted from the fact that the US recovered from the pandemic-related recession faster than the Eurozone, and from the more “hawkish” rhetoric of the U.S. central bank (Fed), which in June, September and December revised upwards the forecasts for the interest rate hikes in the U.S., moving them first from 2024 to 2023 and then to increasing their projected number from 2 to 3 (25 bps each). In Q4 the U.S. central bank also began phasing out its asset purchases. A significant increase in the attractiveness of the US dollar on global markets as a result of Fed's policy translated into an increase in the exchange rate of the American currency against the Polish zloty, which rose from 3.76 to 4.06 (NBP data).

PLN exchange rate (NBP data)

The Swiss franc to PLN exchange rate rose from 4.26 at the end of 2020 to 4.45 at the end of 2021 (NBP data), although during this period it went down even to the range of 4.12. However, both the ECB, by announcing the impossibility of raising interest rates until the end of 2022 (which favored the strengthening of the franc against the euro), and the NBP, by maintaining relatively low interest rates in the conditions of clearly rising inflation, ultimately contributed to the weakening of the zloty against the Swiss franc (as the exchange rate of the franc against the zloty is a cross rate of the euro against the franc and the euro against the zloty: CHF/PLN = EUR/PLN : EUR/CHF).