Climate change research

The PZU Group conducts regular stress tests and sensitivity analyses under its annual analysis of own risk and solvency assessment (ORSA) and stress tests consistent with the requirements of the regulatory authority. Under ORSA, the sensitivity analyses for PZU cover stress scenarios affecting assets and liabilities. The stress tests selected for execution as part of this assessment cover the major areas of activity and the PZU Group’s risk profile. They correspond to the assessment of the most important risks; in particular, the short-term impact of extreme weather-related phenomena (catastrophic losses) and the impact of the growth of the loss ratio on the PZU Group’s capital condition are regularly analyzed.

In addition, PZU as the parent company runs a recurring process to analyze risks and identify key risks in conjunction with the processes of managing the various categories of risk specified in this section in the table entitled Categories of risk in the Group. All of the risks identified during this process are assessed from the perspective of frequency and severity of materialization (taking into account financial severity and reputation impact). In particular, risks related to climate change are subject to risk in terms of physical risks and transition risks. This process facilitates risk analysis in the medium-term and identification and assessment of emerging risks. This analysis is updated at least once a year.

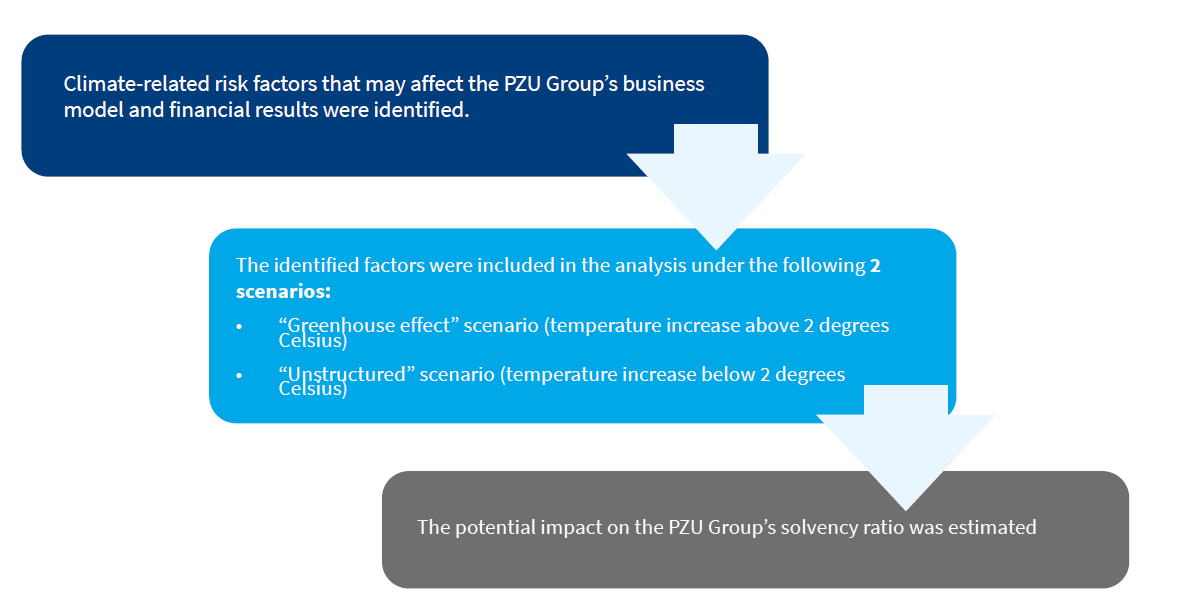

The following climate-related risk factors that may affect the PZU Group’s business model and financial results have been identified as a result of these analyses:

| Risk factor | Horizon | Category of risk in the risk management system | Measures taken | |

| TRANSITION RISKS | The difference between the pace of transforming the Polish economy and the changes transpiring on the reinsurance market leading to constrained availability of reinsurance offers for projects related to the mining industry and the coal-fired power sector. The materialization of this risk may lead to the following consequences: | |||

|

Medium / Long | Business risk (process of analysis of key risks) | Negotiations are conducted with reinsurers and clients when contracts are renewed. Clients see the offered scope of insurance adjusted to the available reinsurance offer. It is necessary to curtail the limits of liability. Additionally, it is assumed that the PZU portfolio will undergo gradual transformation in line with the transition of the Polish economy. |

|

|

Short | |||

|

Medium | Credit risk | Assessment of reinsurers’ credit quality is conducted based on market data, information obtained from external sources, and an internal model. The model divides reinsurers into several classes, depending on the estimated risk level. A reinsurer will not be accepted if its risk is higher than a pre-defined cut-off point. The acceptance is not automatic and the analysis is supplemented by assessments by reinsurance brokers. In the credit risk monitoring process, the assessment of a given entity is updated on a quarterly basis. | |

| Decline in the prices of shares and corporate bonds in selected sectors due to greater regulatory burdens | Medium | Market risk/ Credit risk | Market risk is subject to constant monitoring and internal system of limits. As part of credit risk there is a comprehensive counterparty assessment and limit-setting system (also applicable to industries). Credit risk assessment of an entity is based on internal credit ratings (the approach to rating differs by type of entity). Ratings are based on quantitative and qualitative analyses and form one of the key elements of the process of setting exposure limits. The credit quality of counterparties and issuers is regularly monitored. One of the basic elements of monitoring is a regular update of internal ratings. |

|

| Raising capital requirements as a result of revising the parameters of the standard formula for selected risks | Medium | Compliance risk | The PZU Group follows regulatory changes on an ongoing basis, it participates in consultations and analyzes the impact of changes that are in the process of being introduced or are planned on its capital position. | |

| PHYSICAL RISKS | Intensification of extreme weather-related phenomena | Long | Actuarial risk | The risk management system in the PZU Group allows it to monitor exposures regularly and the reinsurance program in place significantly reduces the potential net catastrophic loss level to acceptable levels without posing a threat to PZU’s financial stability |

| Occurrence of intensive fires in forested areas in suburban communities and in croplands due to the intensifying drought | Long | Actuarial risk | ||

| Heightened mortality ratio among older persons caused by summer heat waves | Long | Actuarial risk | Analysis and monitoring of risk exposure ratios in selected product groups. Actuarial control cycle, i.e. setting suitable assumptions. |

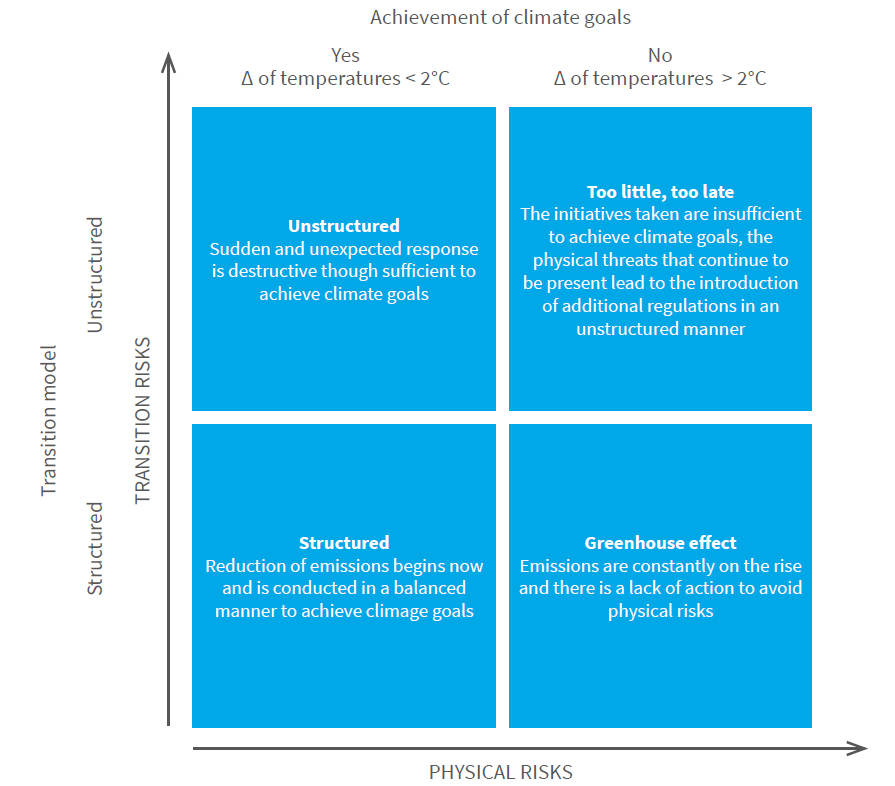

The risk factors itemized in the table above have been analyzed under 2 scenarios for which the starting point is the structure of the scenarios proposed by The Network of Central Banks and Supervisors for Greening the Financial System (NGFS).

Structure of scenarios

Source: A call for action; Climate change as a source of financial risk (April 2019)

Climate-related risk factors analysis

During the current phase of analyzing climate risks the PZU Group studied:

- The “Greenhouse effect” scenario in which physical risks play the main role, which in a simplified approach involve the assumption of a zero impact exerted by transition risks;

- The “Greenhouse effect” scenario in which transition risks play the main role, which in a simplified approach involve the assumption of a zero impact exerted by physical risks.

The below assumptions and risk factors were taken into account:

| “Greenhouse effect” scenario | “Unstructured” scenario |

|

|

The results of this analysis demonstrated that if the assumed scenarios are implemented the PZU Group’s solvency would not be at risk. The regulatory requirements and the assumptions concerning the internal limit system are satisfied in both scenarios. The table below depicts the sensitivity of the PZU Group’s solvency ratio estimated on the basis of forecasts as of the end of 2024.

| Sensitivity of the PZU Group’s solvency ratio |

|

| “Greenhouse effect” scenario | -14 p.p. |

| “Unstructured” scenario | -4 p.p. |

Classifying the occurrence of extreme flooding as a physical risk is the most severe factor. This is a long-term risk associated with temperatures rising more than 2°C. Annual renewals of contracts and analysis of current data and forecasts coupled with the selection of the appropriate reinsurance program make it possible to reduce considerably the possible impact this risk can exert on the PZU Group.

The most severe transition risk is the regulatory risk associated with a change in the parameters used to calculate the sub-module for the natural catastrophe risk.

The extent to which chances and risks related to the climate change will affect the insurance industry depends on a specific product or offered services and the planned investment. The processes of preparation of policies, pricings, reinsurance strategies, as well as the banking and investment activities take into account climate risks based on the short-term perspective. PZU can perceive the potential adverse influence of frequent and increasingly more severe weather phenomena on the financial results. Therefore, PZU incorporates the possibility of catastrophic phenomena in the economic strategies and models it prepares. The goal is to enhance the degree of resistance to the materialization of possible scenarios.

The probability that the risk related to the global economy transition into a low-carbon one (transition risk) will materialize is much higher than the probability that the most extreme physical risk related to the climate change will materialize. PZU takes measures aimed to limit the probability that the transition-related risk will materialize through investments for low-carbon economy. On the other hand, the PZU Group is aware that the materialization of the most extreme physical risk would constitute a threat to the whole insurance sector. The effects of escalating climate changes might contribute to the materialization of risks for which insurance may become unaffordable.

The risk analysis above presents the key risks associated with sustainable development, and in particular climate change. Nevertheless, the response to the identified risks facilitates a change in the direction of a sustainable product offering that does not just correspond to client needs and the identified climate-related challenges but above all that offers an opportunity for business development and building a market edge. The next chapter talks about how the PZU Group shapes its offering and what steps it takes to support preventing climate risks and the Polish economy’s ability to adapt.