Contribution made by the market segments to the consolidated result

The following industry segments were identified in order to facilitate management of the PZU Group:

- corporate insurance (non-life insurance) – a broad scope of property insurance products, liability and motor insurance customized to a client’s needs entailing individual underwriting offered by PZU, LINK4 and TUW PZUW;

- mass insurance (non-life insurance) – property, accident, TPL and motor insurance products offered to individual clients and entities in the small and medium enterprise sector by PZU and LINK4;

- life insurance: group and individually continued insurance – protection, investment (which are not investment contracts) and health insurance; PZU Życie offers it to employee groups and other formal groups, e.g. to trade unions, and persons under a legal relationship with the policyholder (e.g. employer or trade union) enroll in the insurance agreement; individually continued insurance covers persons who acquired the right to individual continuation during the group phase;

- individual life insurance: protection, investment (which are not investment contracts) and health insurance; PZU Życie provides it to individual clients and the insurance agreement applies toa specific insured who is subject to individual underwriting;

- investments – the segment reporting according to the Polish Accounting Standards comprises investments of the PZU Group’s own funds, understood as the surplus of investments over technical provisions in PZU, LINK4 and PZU Życie plus the surplus of income earned over the risk-free rate on investments reflecting the value of technical provisions in insurance products, i.e. surplus of investment income over the income allocated at transfer prices to insurance segments; the segment includes also income from other free funds in the PZU Group, including consolidated mutual funds;

- pension insurance – the segment includes income and expenses of PZU OFE pension funds;

- banking – a broad range of banking products offered to corporate and retail clients by Bank Pekao and Alior Bank;

- Baltic States – non-life insurance and life insurance products provided in the territories of Lithuania, Latvia and Estonia;

- Ukraine – non-life insurance and life insurance products provided in the territory of Ukraine;

- investment contracts – include PZU Życie products that do not transfer material insurance risk and do not satisfy the definition of insurance contract; these are some of the products with a guaranteed rate of return and in unit-linked form;

- other – consolidated companies that are not classified in any of the enumerated segments.

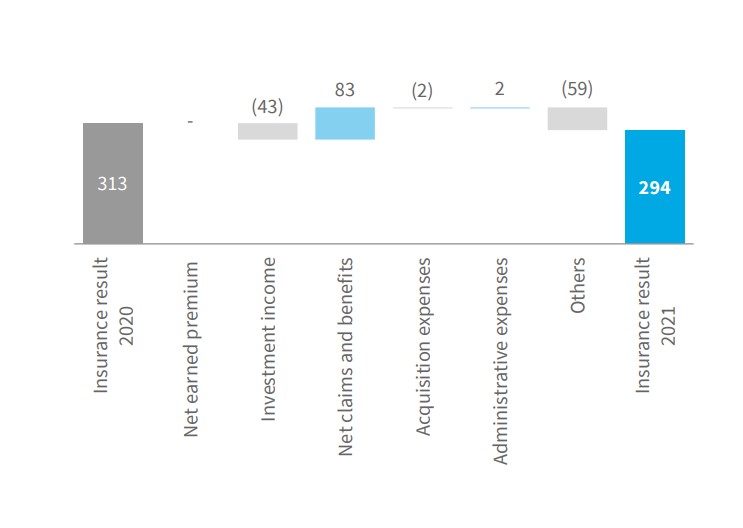

Corporate insurance

The operating result in the corporate insurance segment in 2021 was PLN 294 million, meaning it was down by 6.1% compared to 2020.

The result was affected mainly by:

- net earned premium kept stable at PLN 2,365 million combined with an increase in gross written premium by PLN 257 million (+8.5% y/y) relative to 2020. The growth in gross written premium was driven by:

- premium increase in insurance against fire and other damage to property as the offshoot of signing several high-value agreements, including a renewal of two large contracts, specifically a long-term contract (for 18 months) with a premium of nearly PLN 124 million and an increase in written premium under a contract with an operator in the fuel and energy sector with a total premium in excess of PLN 200 million,

- higher written premium in motor insurance (+1.4% y/y) offered to both leasing firms and in fleet insurance, resulting from the decrease in motor TPL insurance and increase in MOD insurance – as a consequence of the gradual rebound in sales of new vehicles (an increase in new passenger car registrations in 2021 reached 4.3% y/y) and a more rapid growth of the lease market recovering from the slowdown caused by the COVID-19 pandemic,

- improved written premium in the third-party liability insurance portfolio,

- lower sales of insurance against various financial risks and guarantees as a consequence of a decrease in written premium in loss-of-profit insurance;

- drop in the net value of claims and benefits by PLN 83 million (-5.2% y/y), which, combined with the stable net earned premium, resulted in an improvement in the loss ratio by 3.5 percentage points to 63.8%. The decrease in the total loss ratio in the corporate insurance segment was driven by the following factors:

- higher loss ratio in motor insurance, both TPL and MOD. The increased loss ratio resulted mainly from the higher average payout which was partially offset by a lower frequency of reported claims,

- lower loss ratio in the non-motor insurance portfolio, which was a consequence of a better loss ratio in natural catastrophe insurance and various financial risks insurance (in the corresponding period of 2020 a higher loss ratio on the medical entity insurance portfolio);

- the decrease in investment income allocated to the segment on the basis of transfer prices, compared to the previous year, resulted in particular from the depreciation of the euro against the Polish zloty. At the level of the PZU Group’s overall net result, this effect was partly offset by the changed level of insurance liabilities covered by foreign currency assets;

- increase by PLN 2 million (+0.4% y/y) in acquisition expenses (including reinsurance commissions), which, while maintaining the net earned premium at a constant level, resulted in an increase in the acquisition expense ratio by 0.1 p.p. This was chiefly a consequence of changes in the portfolio structure, including a higher share of non-motor insurance and higher share of motor insurance offered under leases (especially noticeable in the first half of the year) and changes in the remuneration model for fleet insurance;

- decrease by PLN 2 million (-1.4% y/y) in administrative expenses, mostly due to the lower costs of protective and preventive measures related to the COVID-19 pandemic compared to initial expenditures during the first year of the pandemic and lower expenditures on advisory services related to strategic and regulatory projects.

Operating result in the corporate insurance segment (in PLN m)

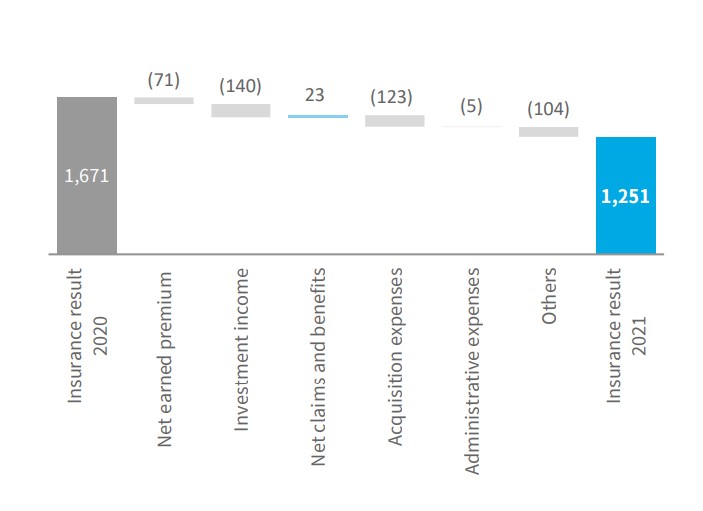

Mass insurance

In 2021, in the mass segment, the PZU Group generated a result of PLN 1,251 million, 25.1% less than the year before.

This was caused by the following factors:

- decrease in net earned premium by PLN 71 million (-0.7% y/y) combined with an increase in gross written premium by PLN 666 million (+6.5% y/y). The PZU Group posted the following under sales:

- increase in written premium in ADD and other insurance, chiefly accident insurance as a result of the growing sales of insurance offered in cooperation with the Group’s banks for mortgage loans and cash loans. The increase was partially offset by a drop in group ADD insurance premiums – in the corresponding period of 2020 insurance cover against a COVID-19 infection was provided to physicians and medical personnel,

- higher premiums from the natural catastrophe insurance and other property damage insurance, chiefly crop insurance (due to the subsidy pool from the state budget greater than the year before), household insurance and insurance for small and medium-sized enterprises. This effect was partly offset by lower premiums from mandatory insurance of farm building insurance due to the significant competition on the market and the natural erosion of the portfolio (declining number of farms),

- higher written premium in motor insurance which, much like in the corporate segment, was caused by weaker sales of motor TPL insurance and an increase in motor own damage insurance (improvement in the number of policies and the average price) – the recovery in sales after a period of lower availability due to the COVID-19 pandemic was partially curbed by the persisting low supply of new vehicles in the market (especially acute in the dealership channel);

- lower net insurance claims and benefits by PLN 23 million (-0.4% y/y), which, when coupled with net earned premium being down by 0.7%, translated into the loss ratio deteriorating by 0.2 p.p. relative to 2020. This change was driven mainly by:

- higher loss ratio in motor insurance, both TPL and MOD, resulting from a higher claim frequency in motor TPL insurance (gradual return to the natural loss ratios after the pandemic period) and a reduction in average payouts,

- lower loss ratio in non-motor insurance, including insurance against fire and other damage to property, mainly as a result of lower than the year before level of losses caused by atmospheric events (ground frosts and hail);

- decrease by 26.7% y/y in investment income allocated to the segment on the basis of transfer prices, compared to the previous year, caused in particular by the depreciation of the euro against the Polish zloty. At the level of the PZU Group’s overall net result, this effect was partly offset by the changed level of insurance liabilities covered by foreign currency assets;

- rise in acquisition expenses (including reinsurance commissions) by PLN 123 million (+6.1%), to PLN 2,133 million, which, when coupled with the net earned premium being down 0.7%, caused growth in the acquisition expense ratio by 1.4 p.p. The increase in acquisition expenses was mainly attributable to the modification in the product and sales channel mix, including a higher share of the multiagency and bancassurance channels;

- increase by PLN 5 million (+0.7% y/y) in administrative expenses as a result of, among other factors, higher personnel costs resulting from the wage pressure, phasing out the aid package for the sales area, weaker demand for advisory services related to strategic and regulatory projects, and lower costs of providing protective and preventive measures related to the COVID-19 pandemic.

Operating result in the mass insurance segment (in PLN m)

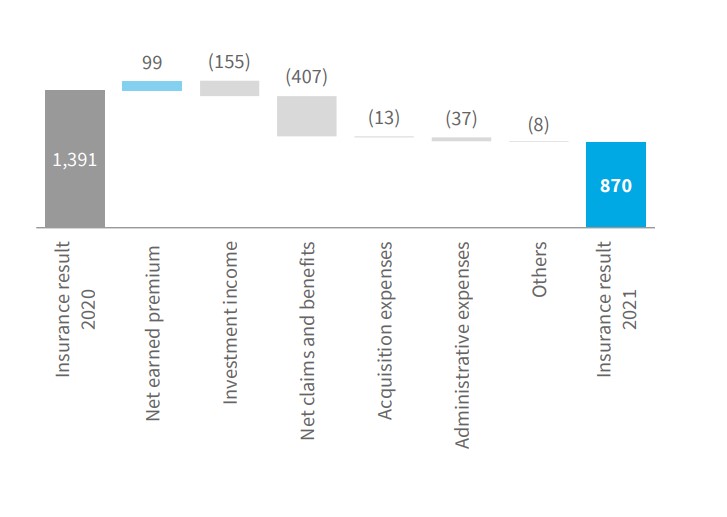

Group and individually continued insurance

In 2021, the operating result in the group and individually continued insurance segment was PLN 870 million, or 37.5% less than in the previous year.

This result was suppressed largely by the increase in benefits triggered by the deaths of insureds and co-insureds observed in the whole population and confirmed by Statistics Poland data.

Factors affecting this segment’s performance and its movements in 2021:

- rise in gross written premium by PLN 23 million (+0.3% y/y) driven by:

- attracting further contracts in group health insurance products or individually continued products (new clients in outpatient insurance and sales of different options of the medicine product) – at yearend 2021, PZU Życie had over 2.5 million active contracts of this type in its portfolio;

- up-selling of other insurance riders as part of individually continued products, including in the malignant neoplasm insurance rider introduced in Q2 2021;

- reduced revenues from group protection products due to the increased attrition of groups of insureds (work establishments),

- increase in the loss ratio control by reducing the pressure on the average premium growth rate in group protection products;

- increase in the net earned premium by PLN 99 million (+1.4%) in connection with the partial derecognition of the provision for unexpired risk established the year before. This provision was established to cover the possible shortfall of future premiums (due to the heightened mortality caused by the COVID-19 pandemic), and its partial derecognition in 2021 was associated with the forecast of a lower mortality rate;

- the decrease in investment income, which is comprised of income allocated according to transfer prices and income from investment products, resulted from deteriorated performance on investment products, especially Employee Pension Schemes, and lower income allocated in protection products. At the same time income from investment products does not affect the result of the group and individually continued insurance segment because it is offset by changes in insurance liabilities;

- higher insurance claims and benefits along with the movement in other technical provisions by PLN 407 million (+7.8% y/y), to PLN 5,597 million. This was caused by:

- rise in insureds’ and co-insureds’ death benefits during the year, corresponding, as follows from Statistics Poland’s data, with a higher mortality in the whole population in the period,

- higher benefits in riders related to hospital treatment and surgical operation and permanent disability and dismemberment as a result of unusually low benefits last year due to lower activity related to the onset of the pandemic,

- growing outpatient health insurance benefits due to low base - limited availability of health care last year caused deferment of some procedures to future periods. The adverse factors were partially offset by a decrease in technical provisions in EPS (a third pillar retirement security product), which was affected by weaker investment performance than in 2020;

- acquisition expenses in the segment of group and individually continued insurance greater by PLN 13 million (+3.4% y/y). This was caused by the higher fees for insurance intermediaries in group protection insurance related to the stronger sales, especially in the segment of insurance products dedicated to small and medium-sized enterprises;

- increase in administrative expenses by PLN 37 million (+ 5.9% y/y), largely caused by an increase in personnel costs as a result of wage pressures, boosting the PZU brand image and higher costs of maintenance of properties due to the indexation of lease prices and utility prices. Factors affecting the decrease in costs included a greater use of vacation leaves (including overdue leaves) by employees, the phasing out of the assistance package for the sales area and lower costs of providing protection and prevention measures related to the COVID-19 pandemic compared to the initial expenses incurred during the first year, as well as weaker demand for renovation work and equipment of the branch network.

Operating result in the group and individually continued insurance segment (in PLN m)

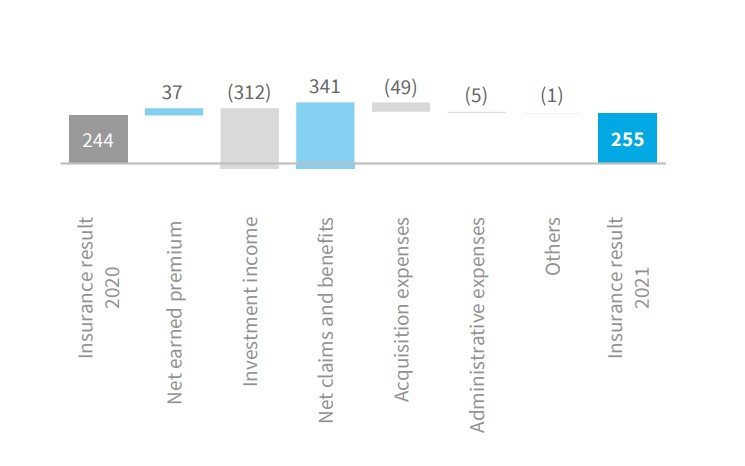

Individual insurance

The operating result in the individual insurance segment in 2021 was PLN 255 million, up by PLN 11 million, or 4.5%, year-on-year.

This improvement was driven by the continued development of protection products in the banking channel and of term products sold in own network.

Factors affecting this segment’s performance and its movements in 2021:

- gross written premium higher by PLN 38 million (+2.2% y/y), to PLN 1,750 million as a result of:

- increase in the portfolio of protection products in the bancassurance channel, including those sold in cooperation with the PZU Group’s banks, chiefly in the area of insurance offered for mortgage loans,

- constantly rising level of premiums in the case of protection products in endowments and term insurance offered in own channels – the high level of new sales and indexation of premiums in agreements remaining in the portfolio,

- decrease in premium generated in investment insurance in the bancassurance channel as a result of restrained cooperation with one of the external distributors. At the same time, positive rates of growth in products offered in collaboration with PZU Group banks;

- the decrease in investment income, which is comprised of income allocated according to transfer prices and income from investment products, was related in particular to the deterioration of funds’ performance in the portfolio of investment products. At the same time income from investment products does not affect the result of the individual insurance segment because it is offset by changes in insurance liabilities;

- lower insurance claims and benefits along with the movement in other technical provisions by PLN 341 million (-20.4% y/y). This was largely caused by a decrease in provisions related to unit-linked products, which resulted both from lower investment income and a slump in contributions to unit-linked funds. From the point of view of the operating result, the latter factor was of small significance – it was offset by a lower level of gross written premium and lower investment income. In turn, the increase in insurance claims and benefits along with the movement in other technical provisions was affected by growth in the protection business carried out in cooperation with banks (where, in connection with single premiums, the establishment of provisions entails high initial costs) and growth in the portfolio of term and endowment products sold in own channels;

- acquisition expenses higher by PLN 49 million (+28.0% y/y), to PLN 224 million. The increase in fees paid to intermediaries for sales of protection products mainly in the bancassurance channel and the additional expenses incurred on sales support in the Group’s own network were partly offset by the lower commissions on sales of unit-linked products in the bancassurance channel;

- increase in administrative expenses by PLN 5 million (+6.2% y/y), largely caused by an increase in personnel costs as a result of wage pressures, boosting the PZU brand image and higher costs of maintenance of properties due to the indexation of lease prices and utility prices. This effect was partly offset by the expiration of the assistance package for the sales area and lower costs of providing protection and prevention measures related to the COVID-19 pandemic compared to the initial expenses incurred during its first year.

Operating result in the individual insurance segment (in PLN m)

Investments

Operating income of the investment segment (based exclusively on external transactions) were higher than in the year before, primarily due to the appreciation of shares in a logistics industry company.

Banking segment / banking activity

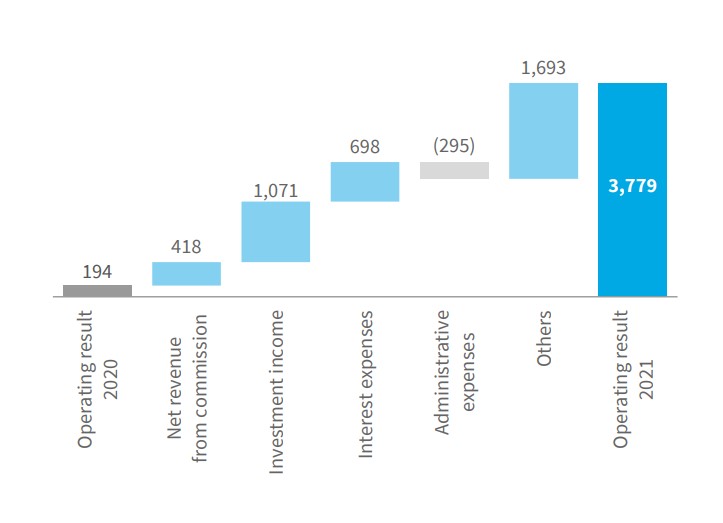

The operating profit in the banking segment (without amortization of intangible assets acquired as part of the bank acquisition transactions), composed of the Bank Pekao and Alior Bank groups, amounted to PLN 3,779 million in 2021 and was higher by PLN 3,585 million than the year before. The result without the impairment of Alior Bank’s and Pekao’s goodwill in 2020 increased by PLN 2,284 million. The higher result was associated mainly with lower costs of risk and higher net fee and commission income.

The COVID-19 pandemic exerted a pivotal impact on the year-on-year comparisons, because it significantly stepped up the cost of risk in 2020, which forced the establishment of additional credit provisions for the forecasted deterioration in the quality of the loan portfolio. Moreover, the decline in banks’ interest income in 2021 was caused predominantly by a series of interest rate cuts throughout the year – by approx. 140 basis points in total, the unfavorable consequences of which were not set off by the increases that followed in Q4 2021.

Bank Pekao’s contribution to the PZU Group’s operating profit in the banking segment (net of the amortization of intangible assets acquired as part of the acquisition transaction) was PLN 3,000 million, while Alior Bank’s contribution was PLN 779 million. Alior Bank’s performance in 2021 was affected by non-recurring events, specifically: the impairment loss on tax assets associated with the Bank’s operations in Romania and the establishment of a provision for commission refunds, the so-called Small CJEU). Moreover, the segment’s performance in the comparable period of 2020 was affected by Alior Bank’s goodwill impairment of PLN 746 million and Bank Pekao’s goodwill impairment of PLN 555 million.

Investment income, being the key component of the banking segment’s revenue, increased to PLN 7,319 million (+17.1% y/y). It consists of interest and dividend income, trading result and result on impairment losses. The increase in investment income was primarily due to lower allowances for expected credit losses due to recognizing additional allowances related to the COVID-19 pandemic last year. This effect was partially offset by provisions for legal risk related to mortgage loans in foreign currencies. An additional impact on investment performance was exerted by the decrease in interest income correlated with the central bank’s interest rate cuts in 2020 by a total of 140 basis points; the subsequent interest rate hikes in Q4 2021 managed to only partially offset the effect of the previous cuts.

The total portfolio of loan receivables in both banks increased by PLN 17.3 billion (+8.7% y/y) in 2021 compared to 2020. In 2021, the value of loans granted to retail customers increased, including mortgage loans, which, given the low rates (for most of 2021), were popular among customers.

The value of allowances for expected credit losses and impairment losses on financial instruments totaled PLN 777 million in Bank Pekao and PLN 1,050 million in Alior Bank, and was lower y/y by PLN 804 million and PLN 686 million, respectively.

The profitability measured by the net interest margin was 2.39% for Bank Pekao and was lower by 6 bps relative to 2020, while in Alior Bank it stood at 3.75%, i.e. 17 bps less than the year before. The difference in the net interest margin level between Bank Pekao and Alior Bank resulted from the structure of the loan receivables portfolio. In both banks, the interest margin declined as a result of the low level of interest rates prevailing for most of the year. The rate hikes announced in the last quarter of the year only partially counteracted this drop.

Operating result in the banking segment (in PLN m)

The net fee and commission income in the banking segment improved by 14.0% relative to the previous year and reached PLN 3,426 million. The main drivers of the improved commission income were commissions on loans, borrowings and leases and commissions on currency exchange transactions.

The segment’s administrative expenses increased to PLN 5,077 million, up 6.2% compared to 2020. For Bank Pekao and Alior Bank, they totaled PLN 3,619 million and PLN 1,458 million, respectively. The increase resulted chiefly from higher costs in Bank Pekao, mainly in connection with the integration of the acquired spun-off portion of Idea Bank, the recovery of variable costs of remuneration and the growing depreciation and amortization associated with investments in the Bank’s transformation.

In addition, other contributors to the operating result included other operating income and expenses, above all the Bank Guarantee Fund fees (PLN 396 million) and the levy on other financial institutions (PLN 965 million). Bank Pekao's result was additionally affected by a restructuring provision in the amount of PLN 120 million in connection with the agreement with the trade unions concerning group layoffs of 23 March 2021, and the decline in other operating expenses in Alior Bank was predominantly caused by the higher expenses incurred in 2020 in connection with the goodwill impairment caused by the acquisition of Meritum Bank ICB SA in the amount of PLN 104 million and the redemption of non-financial assets related to the T-Mobile Banking Services project being closed in the amount of PLN 48 million.

The Cost/Income ratio was 42% for both banks (43% for Bank Pekao and 40% for Alior Bank), or 1.2 percentage points less than the year before. The improved value of the ratio was a consequence of income growing faster than costs. The increase in income was experienced chiefly in the area of commission income.

Pension insurance

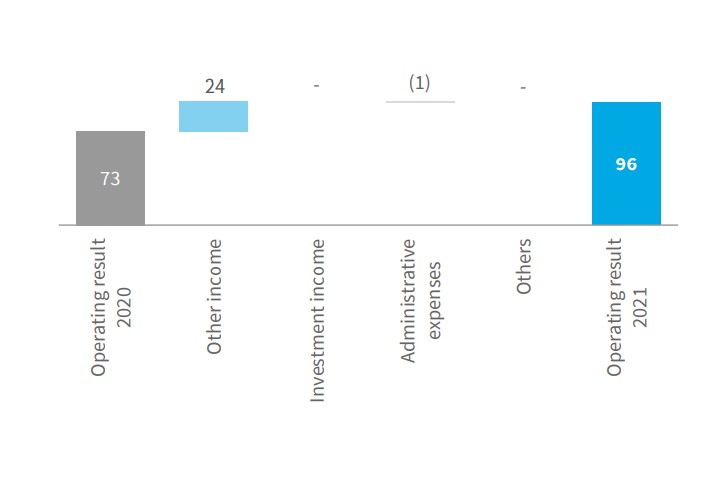

The operating profit in the pension insurance segment amounted to PLN 96 million in 2021, or 31.5% more than in 2020. Factors affecting the operating result and its movement:

- other revenue higher by PLN 24 million (18.5% y/y), to PLN 154 million. It was driven by revenue from the reserve account (PLN 11.6 million) and improved revenue from the management fee;

- administrative expenses higher by PLN 1 million (+1.8% y/y), to PLN 57 million. This was caused by an increase in personnel costs and the costs of marketing and sales support as well as a slight increase in the funds’ operating expenses;

- neither investment income nor other items changed compared to 2020 and stood at PLN 4 million and PLN -5 million, respectively.

Operating profit in the pension insurance segment (in PLN m)

Baltic States

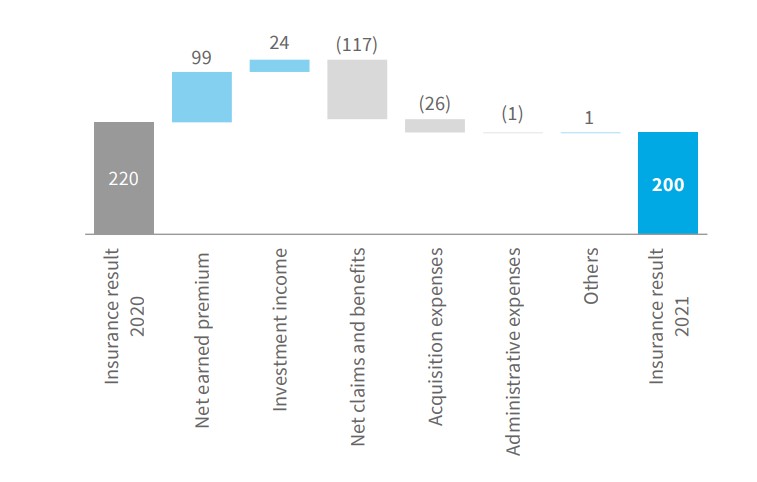

The operating result on the activity in the Baltic States in 2021 was PLN 200 million, down by PLN 20 million, or 9.1%, compared to 2020.

The following factors affected this result:

- net earned premium higher by PLN 99 million (6.0% y/y) combined with an increase in gross written premium. Gross written premium totaled PLN 1,867 million and was higher than the year before by PLN 173 million (+10.2% y/y, +7.7% y/y in the functional currency). Sales were up by PLN 164 million (10.2% y/y), generated in non-life insurance, chiefly as a result of a considerable growth in sales of property insurance (+17.4% in the functional currency), motor own damage insurance (+6.1% in the functional currency) and health insurance (+19.6% in the functional currency). A decrease in sales, as a result of low premium rates across the region, was recorded in motor third party liability insurance (-4.4% in the functional currency). In life insurance, sales climbed by PLN 9 million (+11.1% y/y);

- investment income higher by PLN 24 million, to PLN 42 million, mainly as a result of increases in stock markets;

- net claims and benefits higher by PLN 117 million (12.1% y/y). The previous year’s restrictions caused by the COVID-19 pandemic contributed to a significantly lower frequency of losses in motor insurance and to a lower frequency of disbursed health insurance benefits. In 2021, the situation gradually returned to the pre-pandemic levels – an increase in the frequency of losses and the average loss value was noticeable. The loss ratio in non-life insurance rose 2.4 p.p. to 60.2% compared to the previous year. In life insurance, the value of benefits stood at PLN 87 million and was PLN 26 million greater than in 2020;

- increase in acquisition expenses by 7.6% to PLN 366 million. The rate of growth in expenses was correlated with the rate of growth in sales; the acquisition expense ratio calculated on the basis of net earned premium increased by 0.3 p.p. to 21.0%;

- administrative expenses slightly higher (+0.7% y/y) at PLN 142 million. The administrative expense ratio stood at 8.2%, down 0.4 p.p. compared to the previous year.

Operating result in the Baltic States segment (in PLN m)

Ukraine

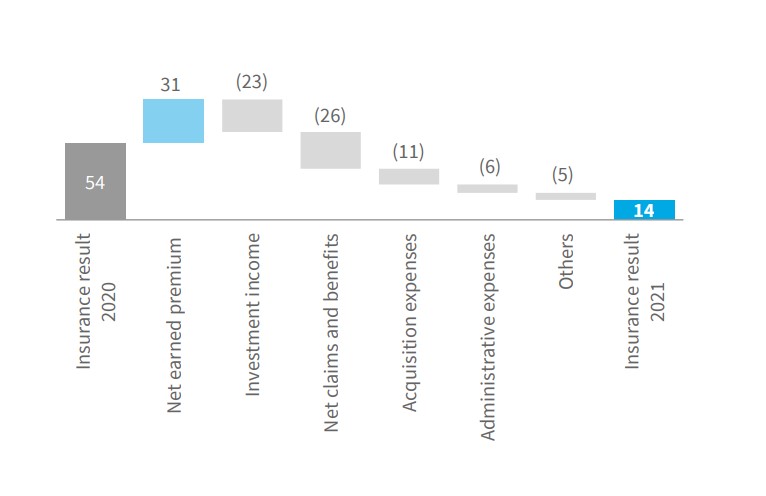

The Ukraine segment ended 2021 with the result on insurance activity deteriorated by PLN 40 million, at PLN 14 million compared to PLN 54 million in 2020. The segment’s result takes into account valuation of the equity stake in PZU Ukraine repurchased by PZU from PZU Ukraine Life (impact on the result: PLN -14 million).

Factors affecting this segment’s performance:

- increase in net earned premium by PLN 31 million (+15.8% y/y) combined with an increase in gross written premium. Goss written premium totaled PLN 339 million and increased by PLN 48 million (+16.5% y/y, +17.6 in the functional currency). Sales in 2020 were largely affected by the restrictions on the movement of people imposed during the COVID-19 pandemic, as a result of which sales of travel and other third party liability insurance policies (mandatory for individuals applying for a visa to travel to Poland) decreased significantly, in line with sales of green card insurance. In 2021, sales volumes of these products increased by a total of 27.9% in the functional currency. Sales of motor third party liability and motor own damage insurance also increased (in total by 15.9% y/y in the functional currency). Written premium in life insurance increased by PLN 13 million (+16.9% y/y);

- investment income lower by PLN 23 million; the value of investment income was burdened in 2021 with the valuation performed for the purposes of the PZU Ukraine share transfer transaction;

- net claims and benefits higher at PLN 102 million (+34.2% y/y). Last year, the restrictions in movement introduced due to the COVID-19 pandemic considerably contributed to the lower frequency of losses in motor TPL and MOD insurance, coupled with a lower frequency of losses in health insurance. In 2021, the frequency rates hovered above levels similar to those recorded in the pre-pandemic period. Moreover, the value of claims was affected by large losses in the corporate client segment. In life insurance the value of benefits paid increased by PLN 1 million (+2.9% y/y) compared to the previous year. The loss ratio calculated on the basis of the net earned premium in non-life insurance was 47.5%, up 13.9 p.p. compared to 2020;

- increase in acquisition expenses to PLN 112 million from PLN 101 million (+10.9% y/y) in the previous year. The rate of growth in expenses is correlated with the rate of growth in sales; however, the acquisition expense ratio decreased by 2.2 p.p. to 49.3%;

- administrative expenses higher by PLN 6 million (+18.2%), at PLN 39 million. The administrative expense ratio calculated on the basis of the net earned premium increased 0.4 p.p. and stood at 17.2%. The increase was caused, among others, by the higher personnel costs as a result of the payroll pressure and the increase in expenses related to the project activity.

Operating result in Ukraine segment (in PLN m)

Investment contracts

In the consolidated financial statements investment contracts are recognized in accordance with the requirements of IFRS 9.

The results of this segment are presented according to the Polish Accounting Standards, which means that they include, among other things, gross written premium, claims paid and movements in technical provisions. These categories are eliminated at the consolidated level.

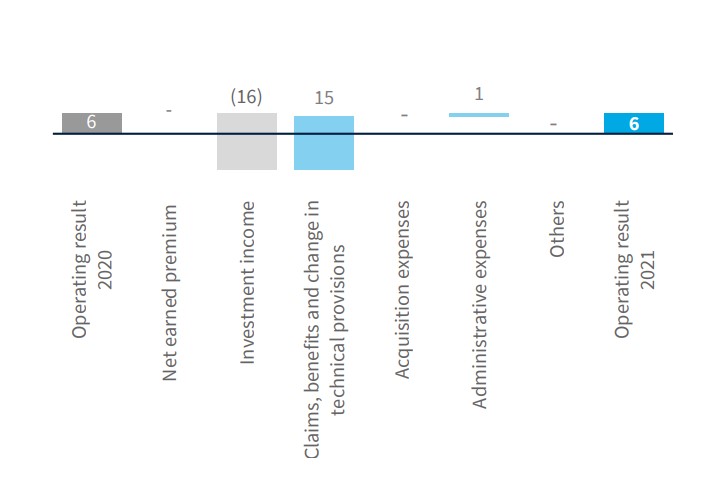

Gross written premium generated on investment contracts in 2021 remained stable compared to 2020, having reached PLN 33 million.

The investment result in the segment of investment contracts deteriorated compared to the previous year, chiefly due to the lower rate of return on individual pension security accounts. Additionally, investment income does not affect the result of the investment contracts segment because it is offset by changes in insurance liabilities.

The cost of insurance claims and benefits together with the movement in other net technical provisions decreased by PLN 15 million (-40.5% y/y) to PLN 22 million, mostly due to the aforementioned difference in investment income in unit-linked products.

In the investment contract segment, no active acquisition of contracts is currently underway.

Administrative expenses decreased to PLN 2 million (-33.3% y/y) as a consequence of the decreasing portfolio of contracts in this segment.

The segment’s operating result remained stable compared to the previous year at PLN 6 million.

Operating result in the investment contracts segment (in PLN m)

Alternative Performance Measures

Selected Alternative Performance Measures (APM) within the meaning of European Securities and Markets Authority Guidelines (ESMA) no. 2015/1415 are presented below.

The profitability and operational efficiency indicators presented herein, constituting standard measures applied generally in financial analysis, provide, in the opinion of the Management Board, significant additional information about the PZU Group’s financial performance. Their usefulness was analyzed in terms of information, delivered to the investors, regarding the Group’s financial standing and financial performance.

Profitability indicators

To facilitate the analysis of PZU Group’s profitability, such indicators were selected that best describe this profitability in the opinion of the Management Board.

The return on equity (ROE) and the return on assets (ROA) indicate the degree to which the Company is capable of generating profit when using its resources, i.e. equity or assets. They belong to the most frequently applied indicators in the analysis of profitability of companies and groups regardless of the sector in which they operate. Return on equity (ROE) is a measure of profitability. It permits an assessment of the degree to which the company multiplies the funds entrusted to it by the owners (investors). This is a ratio of the generated profit to the held equity, i.e. financial resources at the Group’s disposal for an indefinite term which were contributed to the enterprise by its owners. In the case of the PZU Group, the value of net profit and equity differ considerably depending on whether they are provided excluding or including the profit/equity of minority shareholders. Therefore, both return on equity (ROE) – attributable to equity holders of the parent, and return on equity (ROE) – consolidated, without excluding profit and equity attributable to non-controlling shareholders, are presented.

Return on assets (ROA) reflects their capability of generating profit. This indicator specifies the amount of net profit attributable to a unit of financing sources engaged in company’s assets.

Return on equity attributable to equity holders of the parent (PZU) for 2021 was 18.6%. At the same time, it was 7.7 p.p. higher than that achieved in the previous year, which resulted from the improved result in the banking business – in the corresponding period of last year, there was a one-off effect of the impairment loss on goodwill arising from the acquisition of Alior Bank (PLN 746 million) and Bank Pekao (PLN 555 million) coupled with a lower than last year costs of risk stemming from the recognition of additional provisions for expected credit losses. Moreover, the higher return on equity was driven by investment performance in 2021 resulting from the increase in the valuation of shares in a logistics company caused by its admission to trading on the stock exchange.

Return on assets (ROA) of the PZU Group for 2021 was 1.4%, i.e. 0.7 p.p. higher than in 2020. The primary cause was the increase in the result on banking activity, driven by:

- lower cost of risk related to the establishment of additional provisions for expected credit losses last year;

- non-recurring impairment loss on goodwill arising from the acquisition of Alior Bank and Bank Pekao and impairment loss on assets arising from the acquisition of Alior Bank (i.e. trademark and client relations)).

| Basic performance indicators of the PZU Group | 2017 | 2018 | 2019 | 2020 | 2021 |

| Return on equity (ROE) attributable to equity holders of the parent (annualized net profit/average equity) x 100% | 21,0% | 22,1% | 21,2% | 10,9% | 18,6% |

| Return on equity (ROE) consolidated (annualized net profit/average equity) x 100% | 15,3% | 14,6% | 13,5% | 6,1% | 13,0% |

| Return on assets (ROA) (annualized net profit/average assets) x 100% | 1,9% | 1,7% | 1,5% | 0,7% | 1,4% |

Operational efficiency ratios

To facilitate the analysis of PZU Group’s performance, such indicators were selected that best describe performance in the case of insurance companies and those pursuing banking activity in the opinion of the Management Board. Some indicators refer the costs of pursuit of insurance activity to premiums, hence reflect which portion of the premium was allocated to costs and which portion – to margin. For the banking activity, the Cost/Income (C/I) ratio was selected as the relation which best reflects the performance of this area of the activity in the opinion of the Management Board. All indicators are widely applied by other companies from the corresponding sectors and by investors and serve an analysis of efficiency and profitability of these companies.

One of the fundamental measures of operational efficiency and performance of an insurance company is COR (Combined Ratio) calculated, due to its specific nature, for the non-life insurance sector (Section II). This is the ratio of insurance expenses related to insurance administration and payment of claims (e.g. claims paid, acquisition and administrative expenses) to the earned premium for a given period

| Operational efficiency ratios | 2017 | 2018 | 2019 | 2020 | 2021 | |

| 1. | Gross claims and benefits ratio (simple)(gross claims and benefits/gross written premium) x 100% | 67,3% | 63,8% | 66,5% | 67,5% | 64,3% |

| 2. | Claims and benefits ratio on own share (net claims and benefits / earned premium on own share) x 100% | 70,0% | 65,2% | 68,0% | 67,7% | 67,7% |

| 3. | Insurance segment activity expense ratio (insurance activity expenses/earned premium on own share) x 100% | 21,1% | 21,4% | 22,3% | 22,6% | 23,8% |

| 4. | Insurance segment acquisition expense ratio (acquisition expenses/premium earned on own share) x 100% | 14,0% | 14,5% | 15,1% | 15,3% | 16,3% |

| 5. | Administrative expense ratio in the insurance segments (administrative expenses/premium earned on own share) x 100% | 7,2% | 6,9% | 7,2% | 7,4% | 7,6% |

| 6. | Combined ratio in non-life insurance (net claims and benefits + insurance activity expenses) / net premium earned on own share x 100% | 89,6% | 87,1% | 88,5% | 88,2% | 89,2% |

| 7. | Operating profit margin in life insurance (operating profit /gross written premium) x 100% | 19,3% | 21,3% | 20,5% | 18,6% | 12,7% |

| 8. | Cost/Income ratio - banking operations | 48,0% | 42,3% | 40,8% | 43,4% | 42,2% |

In recent years, the combined ratio (for non-life insurance) of the PZU Group’s has been maintained at a level ensuring high profitability of business.

In 2021, it stood at 89.2% and was 1.0 p.p. higher than in 2020, largely due to the higher acquisition expense ratio in the mass insurance segment. The increase in acquisition expenses was mainly attributable to the modification in the product and sales channel mix, including a higher share of the multiagency and bancassurance channels and a lower value of earned premium.

Operating profit margin in life insurance is also an important indicator, i.e. the profitability of life insurance segments calculated as the ratio of the result on operating activity to gross written premium. In 2021, the indicator reached 12.7%, and its fall by 5.9 p.p. in comparison to 2020 was in particular due to a higher loss ratio in group and individually continued insurance. It was attributable to higher mortality resulting from the COVID-19 pandemic.

As regards banking activities, efficiency is measured by the cost to income ratio, i.e. the quotient of administrative expenses and the sum of operating income, excluding: the BFG charge, the levy on other financial institutions and the movements in allowances for expected credit losses and impairment losses on financial instruments. In 2021, the cost to income ratio in the PZU Group’s banking business reached 42.2%, and was lower than in 2020 by 1.2 p.p. due to the rate of growth in income surpassing that in costs. The increase in income was experienced chiefly in the area of commission income.