Polish and Baltic States insurance sector compared to Europe

Insurers operating in the European Union in 2020 raised EUR 994 billion in premiums, representing approximately 18.0% of global gross written premium1.

The year 2020 brought many challenges for the insurance market and required effective management in difficult market conditions. Overnight, insurers were faced with a reduced scale of business as a result of the restrictions put in place to counter the spread of COVID-19. The pandemic has accelerated such processes as the digitization of the insurance market or the automation of processes and changed the way business is done. Proactive adaptation to the new conditions and ensuring business continuity became critical. Processes and projects planned to be implemented over several years had to happen in a short period of time. The introduction of remote work and customer service was associated with increased cyber security concerns, and the economic downturn and continued uncertainty in the labor market did not support positive market sentiments. There were concerns about inflation, increased loss ratio in life insurance and reduced demand for voluntary insurance.

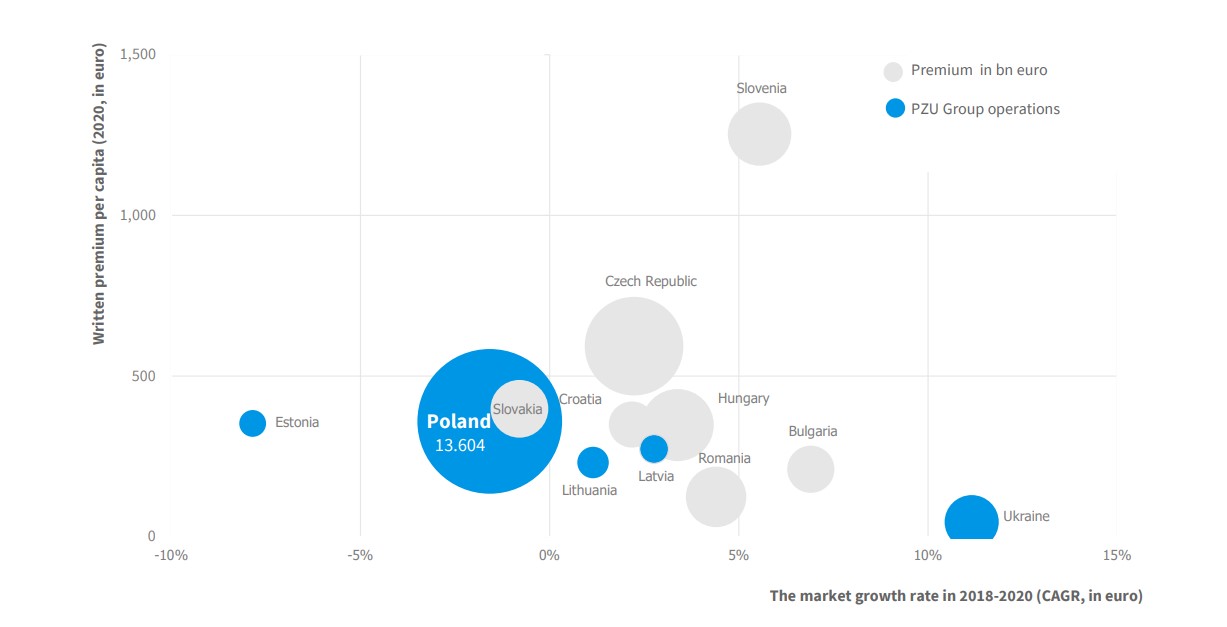

In 2020, the statistical European spent approximately EUR 1,778 on insurance2. A year earlier it was EUR 1,8103. The average Pole spent EUR 359 in 20204, which is nearly 5 times less than the statistical European. Insurance spending by residents of Lithuania, Latvia and Estonia was even lower, at EUR 231, EUR 273 and EUR 3535, respectively. In 2020, the average Ukrainian spent only EUR 46 on insurance6. In Poland, the market insurance model has been developing since 1990. At present, Poland has the largest insurance market in Central and Eastern Europe. Despite intensive market development over the years, it is still significantly behind Western European countries. Gross written premium in the Polish market in 2019 amounted to EUR 14.2 billion7. In 2020, it was EUR 13.6 billion8.

Europe’s largest insurance market is the United Kingdom (with EUR 296,7 billion in gross written premium in 2020). Markets above the EUR 100 billion gross written premium threshold include Germany (EUR 226.5 billion), France (EUR 202.7 billion), and Italy (EUR 141.9 billion). In terms of size, the Polish insurance market also trails certain West European countries with a significantly smaller population than Poland, including Austria (EUR 18.0 billion), Belgium (EUR 36.1 billion), Denmark (EUR 33.4 billion), Finland (EUR 25.3 billion), the Netherlands (EUR 76.7 billion), Switzerland (EUR 55.0 billion) and Sweden (EUR 35.9 billion)9.

The structure of the Polish market is dominated by non-life insurance (approx. 67% of the market), with the majority of gross written premium generated by motor insurance. In 2020, gross written premium collected on motor third party liability insurance and motor own damage insurance accounted for 38% of the entire market’s gross written premium10. The share of life insurance in Poland’s total gross written premium (approx. 33%) was lower than the European average.

Gross written premium per capita (2019, EUR) in relation to the insurance market growth rate (2017-2019)

Source: Swiss Re, sigma 3/2021: World insurance: the recovery gains pace; Eurostat; www.osp.stat.gov.lt; www.fktk.lv; www.andmed.stat.ee

The Baltic countries are characterized by a similar structure of insurance markets. In those countries, life insurance, on average, accounts for less than 30% of total gross written premium11. In Western European countries, the situation is different and life insurance dominates. In 2020, above 41% of insurance premiums in Europe was generated in life insurance and nearly 60% in non-life insurance. Countries with the most developed life insurance market are countries that also have the largest insurance markets. These include Italy (in 2020, life insurance accounted for 73.2% of gross written premium), United Kingdom (70.6%), France (59.1%) and the Scandinavian states: Finland (82.8%), Sweden (76.0%), Denmark (72.8%) and Norway (54.8%)12.

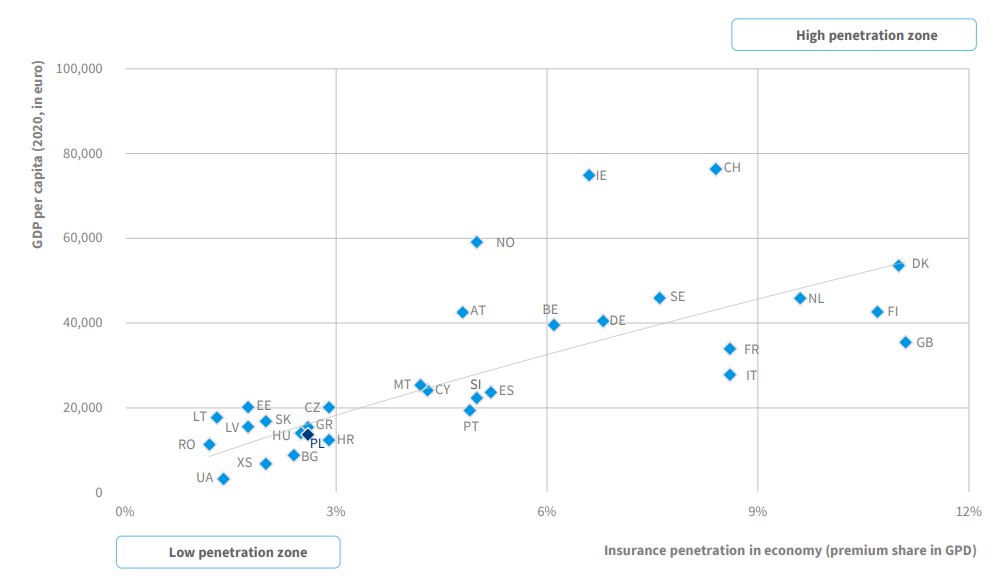

Poland’s insurance penetration rate, which is the ratio of total gross written premium to gross domestic product (GDP), is below the European average. In 2020, this rate stood at 2.6%13, whereas the Europe average was 4.8%14. Even lower penetration rates were achieved in the insurance markets of Lithuania (1.3%), Latvia (1.7%), Estonia (1.7%)15 and Ukraine (1.4%). The highest penetration rates were recorded by the United Kingdom (11.1%), Finland (10.7%), Denmark (11.0%), and the Netherlands (9.6%)16.

Analyzing the penetration of insurance in relation to GDP per capita, it can be expected that the Polish insurance sector will develop alongside Poland’s economic development (growing GDP), greater affluence of the society (increasing disposable household incomes) and growing insurance awareness of the local population, which was exactly the path taken by West European countries.

Penetration of insurance in relation to GDP per capita in Europe (2020, EUR)

Source: Eurostat, Swiss Re Institute (sigma 3/2021)

1,4,6 Swiss Re, sigma 3/2021: World insurance: the recovery gains pace

2 Swiss Re, sigma 3/2021: World insurance: the recovery gains pace; Eurostat; www.osp.stat.gov.lt; www.fktk.lv; www.andmed.stat.ee

3 Swiss Re, sigma 4/2020: World insurance: riding out the 2020 pandemic storm; Eurostat; www.osp.stat.gov.lt; www.fktk.lv; www.andmed.stat.ee

5 Own calculations based on: www.osp.stat.gov.lt; www.fktk.lv; www.andmed.stat.ee

7 Insurance Europe, https://insuranceeurope.eu/insurancedata

8, 9 Swiss Re, sigma 3/2021: World insurance: the recovery gains pace

10 KNF, Biuletyn roczny. Rynek ubezpieczeń 2020, data aktualizacji 28.09.2021r

11 Own calculations based on: www.osp.stat.gov.lt; www.fktk.lv; www.andmed.stat.ee

12, 13, 16 Swiss Re, sigma 3/2021: World insurance: the recovery gains pace

14 Own calculations based on: Swiss Re, sigma 3/2021: World insurance: the recovery gains pace; Eurostat; www.osp.stat.gov.lt; www.fktk.lv; www.andmed.stat.ee

15 Own calculations based on: Eurostat; www.osp.stat.gov.lt; www.fktk.lv; www.andmed.stat.ee