External environment in the Baltic States and Ukraine

Lithuania

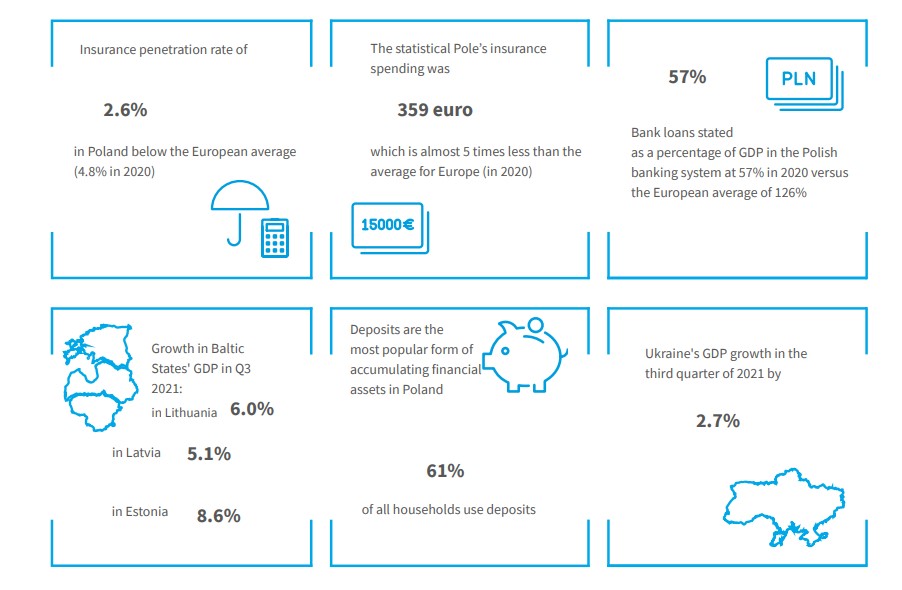

Q3 2021 saw a 6.0% y/y increase in GDP not adjusted for seasonality. It is expected that the strong economic growth figures, the favorable economic outlook of the European Union, and the increased proportion of people who have achieved resilience suggest that economic growth will continue in the medium term.

The labor market situation improved in 2021. With the lifting of the quarantine in the country and the easing of contact restrictions, more people entered the labor market in Q3, resulting in increased labor force participation and employment driven by strong demand for labor, while the unemployment decreased. Industrial production was the sector most conducive to increase in employment in the first three quarters. Increase in employment has brought the nationwide unemployment rate closer to pre-pandemic levels. According to Labour Force Survey data published by the Lithuanian Statistical Office, the country's unemployment rate was 6.7% in Q3 2021. Both the private and public sectors have faced the problem of labor shortages. The number and level of vacancies at the country level is the highest since the first quarter of 2008. At the same time, increased labor shortages can increase the wage pressures and contribute to factors that limit the growth of production.

Favorable economic conditions and strong demand for labor stimulated salary growth. Wages grew at the same rate in both the private and public sectors. Annual wage growth was recorded in all types of economic activity, including the hospitality sector, leisure and retail activities most affected by the pandemic, where wages grew at double-digit rates. Wage growth was driven by a number of factors, including favorable economic development, the ability of business to adapt operations to the pandemic and quarantine conditions in a short period of time, a strong increase in the supply of vacant jobs and a shortage of skilled workers to meet labor market needs, government measures to support stimulation of domestic demand and the minimum monthly wage increased by 5.8 percent.

Steadily rising throughout the year, inflation reached 10.7% in December. The rise in inflation reflects increases in energy prices and disruptions in the supply of raw materials and commodities. It is expected that the main inflation driver will remain the increase in the prices of imported energy commodities, if their prices stabilize, inflation should slow down not only due to a more favorable development of energy commodity prices (transport fuels, thermal energy), but also as a result of the decreasing pressure of energy prices on the cost of production of goods and services.

2021 was a favorable year for exporters. The increase in goods exports was primarily driven by the production of the chemical industry, which accounts for 14.9% of Lithuania's total goods exports. The growth of Lithuania's exports was also influenced by the recovery of demand for petroleum-based products and a strong increase in global oil prices, which led to a rapid increase in exports of mineral products.

Latvia

In Q3 2021, GDP grew by 5.1% y/y (data adjusted for seasonality), overcoming the crisis much faster than expected at the beginning of the year. This has been driven by the favorable situation in external markets as well as by wide-ranging economic support measures, protecting companies and jobs and providing support to the most affected groups of population. However, in Q4, with the rapid spread of the COVID-19 pandemic and new restrictions imposed in early October, economic growth slowed down again and the downturn risk increased significantly.

From the sectoral perspective, trade, health care and social welfare, as well as manufacturing had the largest positive impact on Latvia's economic growth in the first three quarters of 2021. In contrast, declines were recorded in agriculture and construction. The hospitality sector, which has been hardest hit by the restrictions imposed to limit the spread of the COVID-19 pandemic, saw a 12.2% decline in the first three quarters of the year, while arts, entertainment and recreation fell 10.4%. A key role in the recovery was played by the 4.6% growth of private consumption, driven by the gradual easing and lifting of COVID-19 pandemic-related restrictions, as well as support for affected businesses and households. Government consumption also grew strongly, rising 4.9% in the first three quarters of the year, and investments rose 4.9%.

In 2021, consumer prices kept rising. Annual inflation in December was 7.9%, the highest since April 2009. The sharp increase in prices was mainly due to energy shortages. The price of electricity in Latvia was 32.7% higher than in the corresponding period of the previous year. Gas and fuel prices increased by 40.4% and 30.3%, respectively. The future inflation growth rate will be driven by changes in commodity prices, especially energy prices on global exchanges, as well as the situation related to the spread of the COVID-19 virus.

Average gross monthly wages, which rose 6.2% in 2020 despite the COVID-19 pandemic crisis, grew even faster in 2021 as large numbers of low-wage earners were laid off and the minimum wage increased to EUR 500. In Q1 2021, the average monthly gross salary increased by 9.5% compared to the corresponding quarter of the previous year, in Q2 it increased by 10.2% and in Q3 by 10.4%. In 2021, changes in average wages were significantly influenced not only by changes in employee compensation, but also by structural changes in the labor market - the growth of start-ups and closures and changes in the number of employees.

Estonia

Estonia's recovery pace has been one of the fastest in Europe, but its previously dynamic growth has faltered. In Q3 2021, Estonia's annual GDP growth rate stood at 8.6%. At the same time, the Bank of Estonia's economic forecast predicts that this growth will slow down to below 3% next year. It is expected that the further growth in the economy will be more difficult to achieve, and the economy's growth rate will be reduced by exceptionally high inflation. The sectors most affected by the restrictions implemented in the wake of the COVID-19 pandemic, particularly tourism, leisure and hospitality, have not yet returned to pre-pandemic levels, but most industries are doing well.

The consumer price index was 12.0% for the year. Inflation in December was the highest in 20 years. Half of the total price increase in the consumer basket came from energy; electricity and gas prices were more than 120% higher in December than a year earlier. The pass-through of energy costs to final prices of other goods and services is expected to drive inflation in the months ahead.

The unemployment rate was 6.2% at the end of 2021, registering a decrease of 0.8 p.p. compared to December 2020.

Ukraine

Thanks to high domestic demand in 2021, gradual recovery of the economy continued in Ukraine. At the same time, there are still risks of increased quarantine in Ukraine and the world, as well as a more sustained and more significant increase in inflation than expected.

In Q3 2021 Ukraine's GDP grew by 2.7%. Economic growth in the third quarter was primarily driven by stable consumer demand and was tempered by a negative contribution of net exports. Private consumption in Ukraine in the nine months of 2021 accounted for 72.4% of nominal GDP.

In September 2021, the annual inflation rate stood at 7.5%. Stable consumer demand, rising production costs and high global commodity prices remained the main factors accelerating the increase in the consumer price index.

The level of unemployment in Q3 2021 stood at 9.1%.

After nine months of 2021, a foreign trade deficit in goods and services (USD 1.2 billion) was recorded. Its value was, however, lower than a year ago due to a more dynamic growth of exports of goods in comparison with imports.